A mortgage is the smartest way to owning a home

December 3, 2022

Credit Fundamentals will continue discussing some debt criticisms, namely personal finance personality Dave Ramsey’s idea of “living without credit” and why this can make one’s life more difficult than that of a person with credit.

While the previous issue covered this topic in the context of credit cards, I will discuss it in terms of renting and mortgages in this penultimate issue.

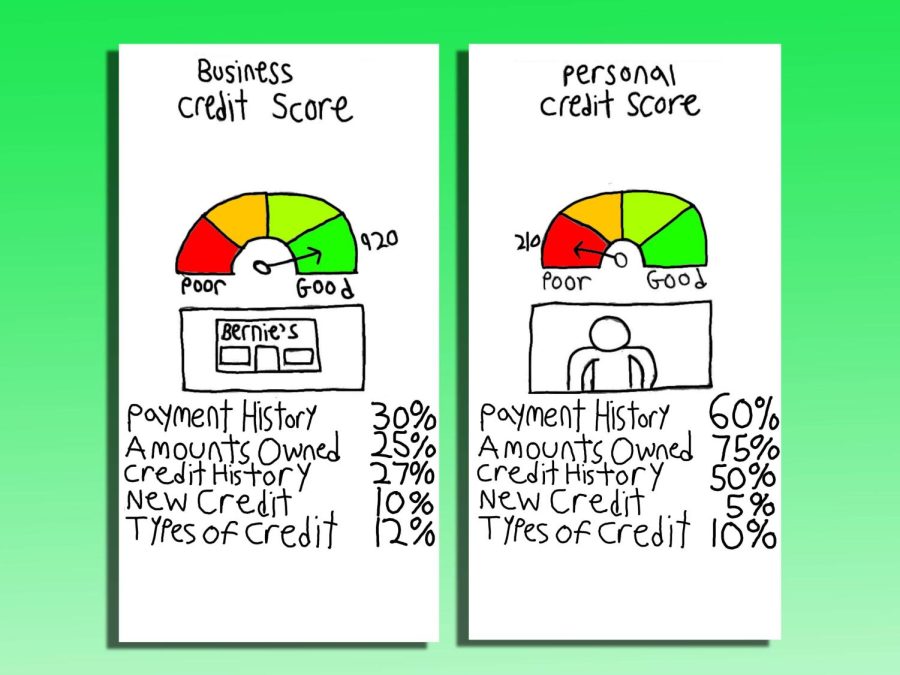

Your FICO score is an important factor in an application to rent out an apartment or obtain a mortgage. In this scenario, no credit has the same effect as bad credit.

You will get denied without special considerations, which can take time to gather.

For example, if you rent out an apartment with no credit, you will be required to dig into your bank statements for proof of rent payments. You may also be required to provide a letter of recommendation from a past landlord.

If the apartment application is more stringent, you may even need a cosigner or a larger security deposit. This is not something everyone can afford.

For mortgages, it is worse. In most cases, you need to put up a larger down payment in the absence of credit. You also pay higher interest rates for the perceived risk of not having experience with debt.

Additionally, not all mortgage lenders offer manual underwriting without a credit score, so you may be immediately denied as soon as you apply.

To people looking to buy a home, Ramsey recommends being patient, suggesting potential homebuyers “rent for a while if you need to and save up even more for a down payment,” in a statement on his website.

Ramsey also suggested skipping the mortgage process and paying immediately in cash, adding that “cash is king.”

Analysts from Real Estate Witch found that the average home value has soared 118% since 1965, going from $171,942 to $374,900. When adjusted for inflation, average incomes rose only 15%, from $59,929 to $69,178.

Using these figures, a household would have to save for five years straight without spending a single penny to afford an average-priced home on an average-sized income. Cash is not “king” when you have to save this much of your income for a house.

Additionally, renting out an apartment will give you no equity in the place you live. Mortgages, however, do provide such equity.

It’s perplexing how Ramsey is comfortable with the idea of renting a place you’ll never own. It would be a much more reasonable investment to obtain a mortgage and build equity in the process, which may lead to generational wealth and price appreciation.

Unless you work at a place that offers a high salary like an investment bank, there is no way your yearly income can support buying a house in cash. Even if you do have that money, you can take out debt at a low interest rate and invest the rest at a higher rate of return.

With the next issue being the last of the semester, I look forward to getting a little more personal in the last edition of the Credit Fundamentals column.