Maximize — but don’t max out — these business credit cards

October 28, 2022

In last week’s issue, Credit Fundamentals covered elusive “invite-only” cards. For Issue 7, I will talk about cards that require some extra steps but are relatively easy to get — business credit cards.

Business credit cards have two main benefits.

For one, these cards usually have higher credit limits compared to personal credit cards. As a single entity, a business tends to make more than a person.

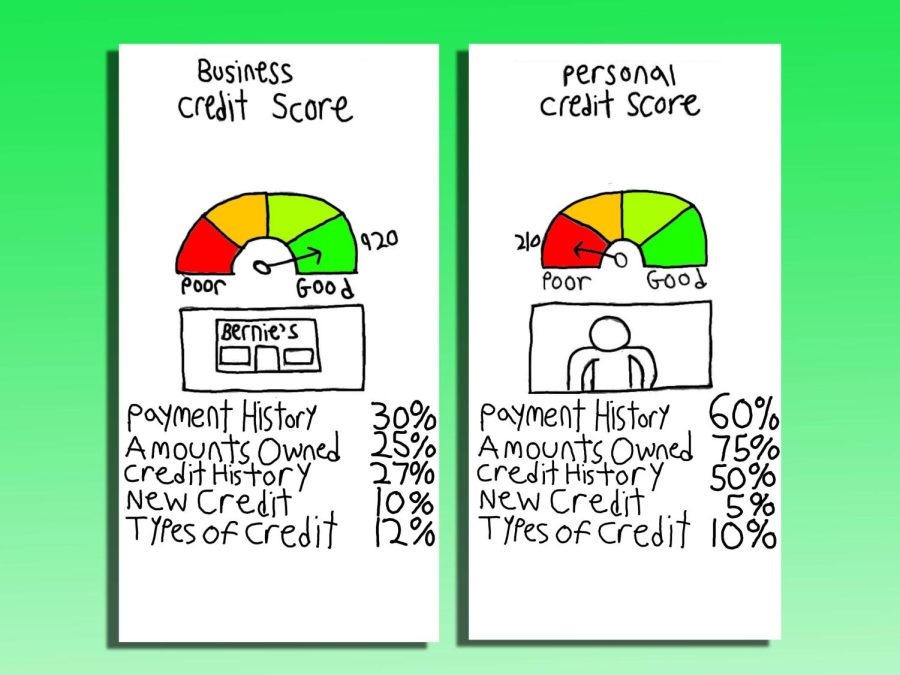

Additionally, business credit is separate from personal credit. If your business is incorporated under a structure that allows for limited liability and happens to go bankrupt, your personal credit and assets will not be affected.

Individuals may qualify for business credit cards without incorporating a business. For example, sole proprietors or freelancers qualify for business credit cards.

But this does present more liability, and lenders often use your personal credit report to check and conduct inquiries in the absence of a business credit report. If you apply for business credit without incorporating a business, you would apply under your social security number, and a bank would run your personal credit.

But if your business is large enough and you incorporate it, you can use an employer identification number. An EIN keeps personal and business expenses private. It also eliminates the need of a “personal guarantee,” which is a promise that you must pay off business cards with personal funds if the business cannot pay it of

1. Chase Ink Business Preferred

JPMorgan Chase & Co.’s Chase Ink Business Preferred card is a strong option.

The card offers a lucrative sign-up bonus of 100,000 points after spending $15,000 in three months. It comes with an annual fee of $95. It also earns three-times cash back on advertising costs, cable service, internet service, phone service, shipping purchases and travel expenses.

This card also earns “ultimate rewards” points, meaning you may combine points with a personal Chase Sapphire Reserve card and receive 1.5-times more in point redemption value through Chase’s travel portal.

In addition, there are unlimited employee cards. If you are a business owner, all business-related purchases your employees make are cash back for you.

2. Amex Blue Business Cash

For a business card with no annual fee and a solid earnings structure, American Express Co. offers the Amex Blue Business Cash. The card rewards user spending gradually, with cash back benefits totaling $250 after $5,000 in spending and an additional $250 after $10,000 in spending.

After those sign-up bonuses, it earns 2% cash back on all purchases up to $50,000, then 1% after that. This is a card for a business owner who values simplicity and wants good value without having to think too much.

This is the fifth and last issue detailing credit cards, since I covered every major category. Hopefully, my credit card recommendations gave you ideas on what perks and points credit can offer you.

We will focus more on the two “L” words in the upcoming issues — leverage and loans — and how they fit into prospective capital structures of a business.