The five factors of a credit report

September 10, 2022

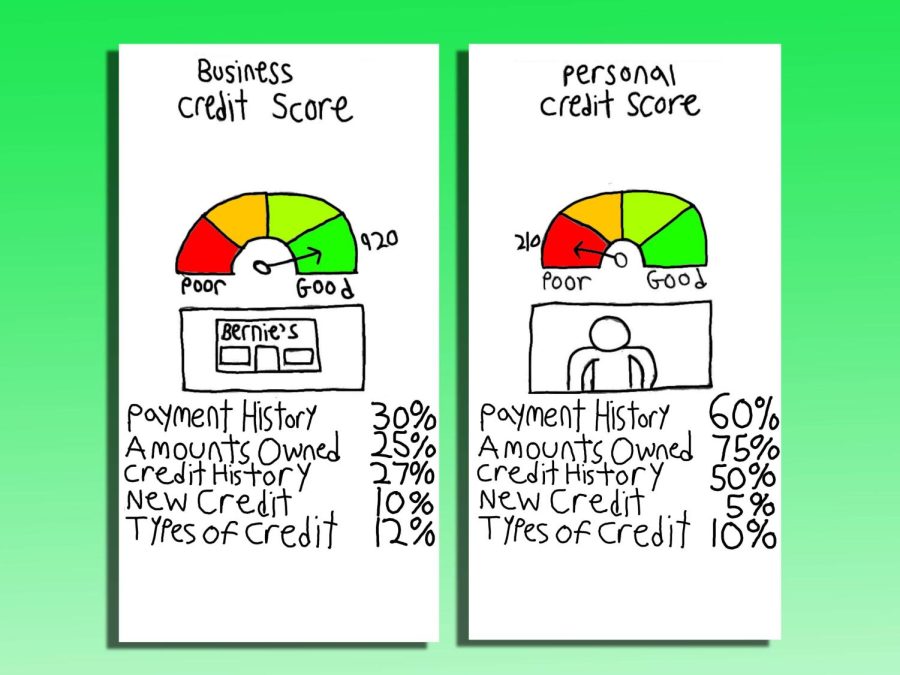

Understanding the foundational five factors of a credit report is a necessity when learning about credit. These five factors are equally applicable, no matter where someone may be in their credit journey, so it is important to remember them.

1. Payment History

Payment history constitutes 35% of one’s overall credit score. Banks want to see that clients are making punctual and consistent payments.

A missed payment on one’s credit report is a huge red flag. To banks, this indicates that they may not get the money they lend clients back. Even one late payment can drop one’s credit score by at least 50.

One good way to keep up with your payment history is to turn on auto-pay on all credit cards held to ensure a payment is not forgotten about. Another way is to use a credit card as if it was a debit card. People should never be charged more than what’s in their bank account.

2. Amounts Owed

The “amounts owed” category makes up 30% of a credit score. It indicates how much outstanding money they have relative to their credit limits. Banks don’t want clients to use the whole credit line they issue out to them, but rather they want it under a special, magic percentage, which is also 30%.

This means that for a credit line of $1,000, one should use $300 or less for a good rating in this category. Having 10%, or in this case $100, is ideal.

A higher credit limit gives people more leeway. This is a reason why older people have higher credit scores. They have more credit age with higher limits, which leads to lower credit utilization.

It should be noted that the 30%-and-under rule should be followed for individual lines of credit and not total credit limit, so don’t max out credit cards.

3. Credit History

The length of one’s credit history accounts for 15% of a credit score.

The easiest way to think about credit history is through an analogy: if someone were to receive open-heart surgery, would they choose the doctor who has been practicing for 30 years or one who has only been practicing for a year? They would go for someone with more experience.

Would a bank rather lend to an experienced 40-year-old with a $150,000 salary or a college kid who does not have a stable job? Banks use the same logic when it comes to issuing loans.

Thus, it is advisable to open a secured credit card once someone turns 18 years old. By doing so, one would have a decade of credit history before turning 30.

4. Credit Mix

Credit mix accounts for 10% of the score. Banks find it more attractive when clients have a good mix of credit products.

There are two main types: revolving, which includes credit cards, and installment, which includes student loans, mortgages and auto loans. It signals to banks that clients have experience managing different types of credit products.

Since credit mix accounts for a low percentage of the overall credit report, people should not take out a loan just for a credit score boost.

5. New Credit

New credit makes up 10% of the score. Banks don’t necessarily see opening 10 credit cards in two months as a good sign. The bank would instead wonder why that person needs all that new debt.

Each time a person applies for new credit, a hard inquiry is made on their account — that is, whether they got approved for the specific product. Hard inquiries stay on a credit report for two years but stop impacting a credit score within a few months. People should be reasonable and space out their credit card applications.

When buying a car at a dealership, come with financing ready, be it an auto loan pre-approval from a bank or credit union. If not, the dealership will prod for a better rate and give clients a bunch of hard inquiries on their account. This should be avoided to take care of a credit score.

Next week’s column will focus on credit products and their different features. Until then, take care of that credit score.