An introduction to Credit Fundamentals

September 3, 2022

People say to give credit where credit is due. It is funny then, that credit does not get any credit for what it can do. Whether it is from their mom or personal finance personality Dave Ramsey, people have heard it all before: “Credit is bad! Cash all the way!”

Being irresponsible with credit can lead to disastrous consequences, but taking a disciplined, methodical approach to credit is an important tool in everyone’s personal finance arsenal.

Having good credit saves people interest on loans, gives access to more favorable credit products and is even a requisite for some jobs — this goes out to all the fellow finance majors.

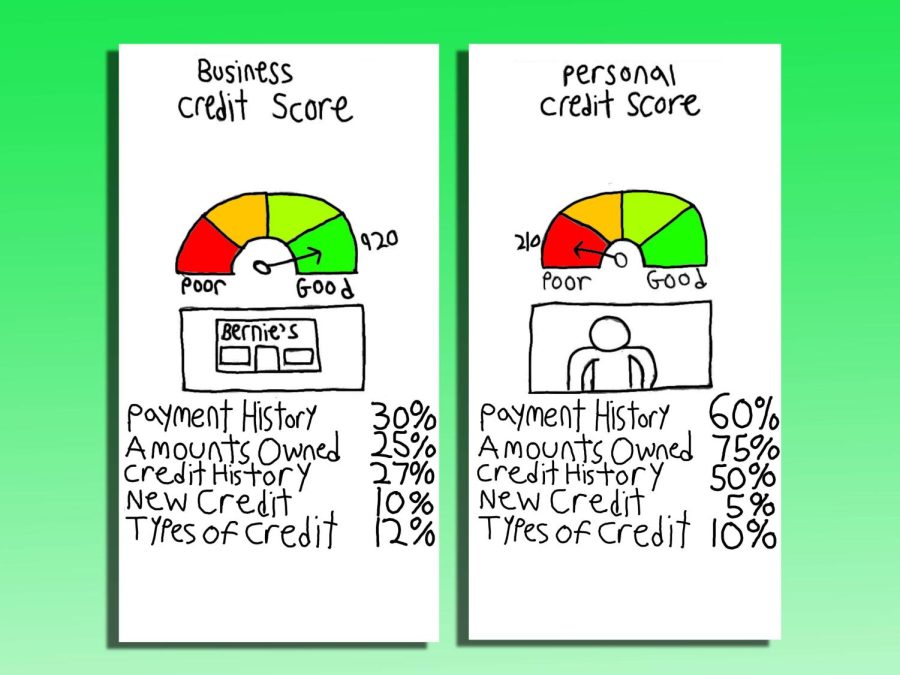

The goal of The Ticker’s new Credit Fundamentals column is to introduce readers to the fundamentals of credit and, in turn, properly set you up for the best chances of success in the realm of credit. This column will go over concepts such as credit score; factors of credit; different lines of credits and their categorizations; and differences between personal and business credit.

After all of these concepts are fully explained and the foundation is laid, perhaps this column will take a more fun approach and go over benefits such as credit card points and exclusive lounges for certain credit cards.

The first point that needs to be stressed about credit is research. This goes for everything, from picking a credit card product that fills one’s needs, to reviewing the terms for a mortgage and seeing how much interest one is paying.

People want to make credit work for them, and not the other way around, so they must ensure the credit they use makes sense, and most importantly, benefits them.

The second important concept to know is that investing and credit have a common principle — the sooner one starts, the more fruits produced.

With investing, people have the benefit of compound interest, which piles up and creates a snowball effect that boosts gains. Credit is similar.

Another important factor is credit age. If one was to open a card at 18, then by 28, they would have a decade of credit history, which equates to a great credit score.

This means that readers do not have to wait for this column to gather information on credit to get the benefits as soon as possible. But, if readers do wait, this credit column will give them all the information they need to start on their credit journey.

Next week’s column will be on the five factors of credit and how each one plays into the overall mix of credit score. Remember to take care of that credit score.