Because of the changes, FICO estimates that about 110 million consumers will see small changes of less than 20 points to their scores under the new credit score model.

This is due to the increased demand by lenders to pinpoint risky borrowers who appear more creditworthy than they are.

Originally, FICO scores were dedicated by your payment history, credit utilization ratio, age of credit and derogative information, which account for 35%, 30% and 15% respectively.

Now the scoring model will judge more harshly on those who miss payments, having rising debt levels, or who pursue credit very rampantly.

However, those with student loans will be treated with more forgiveness. “Don’t panic if you have a lot of student loans and/or a mortgage. Installment debt is almost benign to your credit scores,” said John Ulzheimer on CNBC Make It, an expert on credit scores and credit scoring.

“You can have hundreds of thousands of dollars of installment debt and still have elite credit scores,” he stated. The most noticeable change that will impact many Americans across the country is the flagging of consumers who sign up for personal loans.

The unsecured loans have surged over the past couple of years. In 2018, lenders extended $81.9 billion in personal loans in the first half of the year.

Lenders have been balancing loan volume and risk of the concern about the longevity of the economic recovery.

This isn’t the first time FICO updated its scoring model. Every so often it does so to reflect changes in consumer borrowing behavior and performance. The last time this was done was in 2014. That time, the update was viewed as helping to boost scores.

Dave Shellenberger, the FICO vice president of product management stated, “In fact, consumers who have been good at managing their credit, regularly paying bills on time and keeping their balances in check are likely going to be ‘rewarded’ by seeing a gain in their score under the new model.”

The credit bureaus TransUnion, Equifax Inc. and Experian PLC are also known to rollout programs or aid to help boost scores.

Most recently Experian came out with Experian boost, which helps use positive utility and cell phone bill payment history to increase scores.

As Americans plunge deeper into debt it can be easy to say the changes will hurt many.

Despite low consumer loan losses compared to the 2008 financial crisis, many are relying on debt to help paying for their everyday needs.

Consumer debt was on pace to top $4 trillion dollars. This includes credit cards, auto loans, student loans and personal loans. Homeowners owed a staggering $10.3 trillion on mortgages.

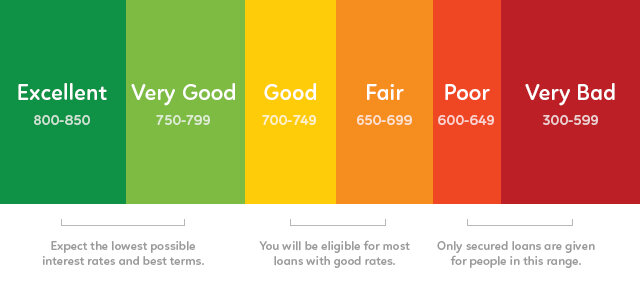

It is very important to have a high credit score as there are a plethora of benefits.

The benefits readily seen are lower interest rates on mortgages, auto loans and lower insurance payments.

Additionally, some employers check credit scores in the recruiting process.

In 2017, those with fair credit paid on average 36% more for their homeowner’s insurance than those with good to excellent credit.

The trick for great financial health moving forward will be the same as it always was.

Obtaining a high credit score is possible by managing credit responsibly, paying bills on time, buying only the necessities and living with little to no consumer debt.